Here is a comparison of the VAT return form valid until 30 June 2025 and the new form valid from 1 July 2025. The new form will be used for the first time for the tax period of July 2025, or the third quarter of 2025, respectively. It was published under Notice MF/007833/2025-731 of 21 March 2025 in the Financial Bulletin no. 9/2025.

How do the forms differ?

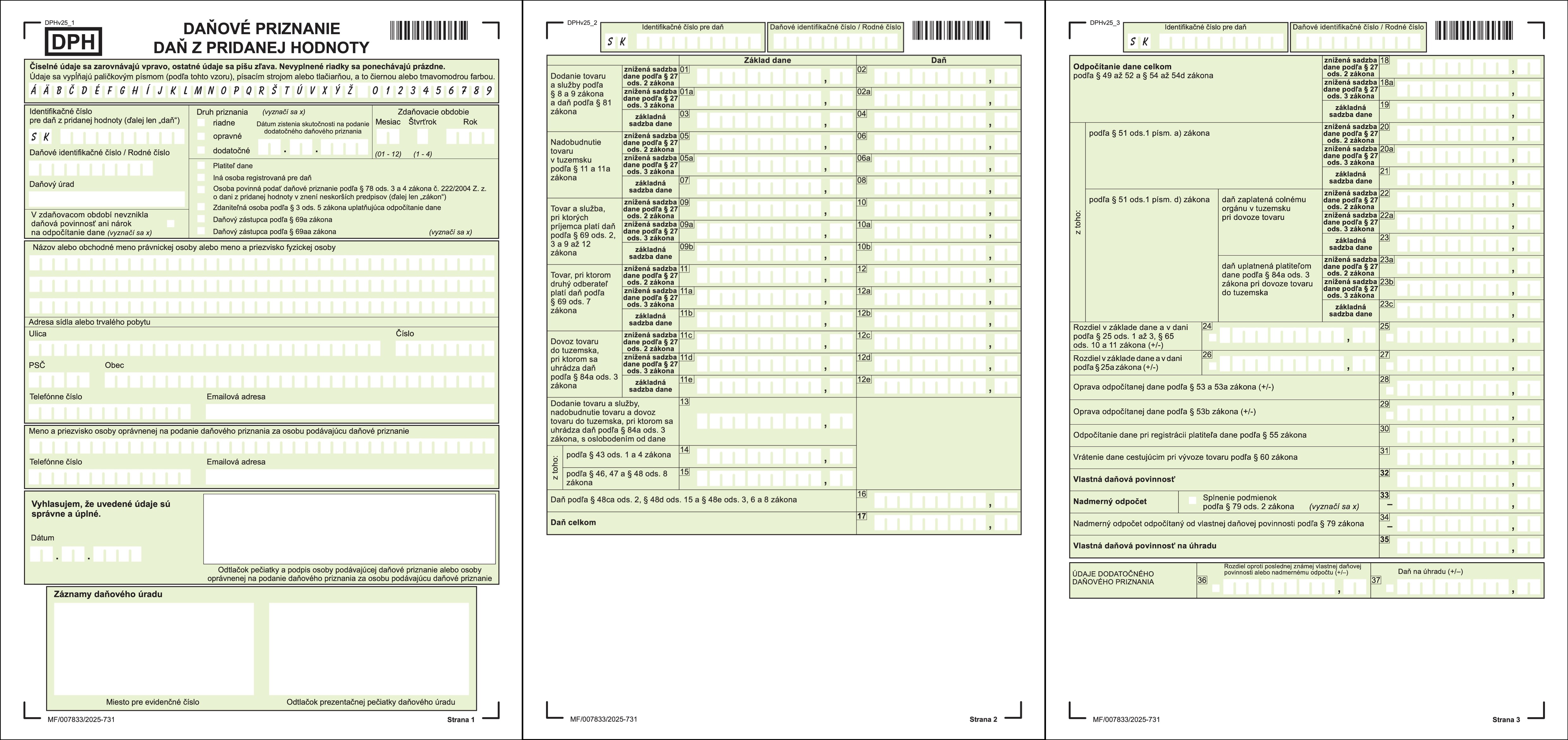

The new form is marked with the code DPHv25_1 in its upper section.

Changes on the first page

Only one change has been made to the data on the first page: the removal of the person filing the tax return under Section 78 (9). This is related to the fact that from 1 January 2025, the VAT Act was amended, changing the method of retroactive filing of tax returns in the event of a late VAT registration.

Changes on the second and third pages

- On the second and third pages of the form, lines have been added for each type of transaction so that a separate line exists for each tax rate. For comparison, in the form valid until 30 June 2025, some transactions were only broken down by "standard rate" and "reduced rate," and the lines for the "reduced rate" included data for both the 5% and 19% tax rates. Some transactions were not broken down by tax rate at all.

- Further changes in the form result from an amendment to the VAT Act and the introduction of self-assessment on importation from 1 July 2025. Lines 11c and 12c (for the 19% tax rate), 11d and 12d (for the 5% tax rate), and 11e and 12e (for the 23% tax rate) have been added.

- For the deduction of tax from self-assessment on the importation of goods, lines 23a, 23b, and 23c have been added, each for a specific tax rate.

- On line 13, importation with self-assessment, which is exempt from tax, has been added to the list of exempt transactions.

General changes and retained features

- The new form has three pages instead of the original two.

- The added lines are distinguished by letters; for example, the 'own tax liability' to be paid can still be found on line 35.

- Lines 24 - 37 remain unchanged.

- The tax rates on the form are identified by reference to the provisions of the VAT Act, meaning that if the rates change in the future, it will not be necessary to change the form again.

If you have any questions regarding the new VAT return form, please contact us.

Be the first to know about the latest information from the world of taxation, accounting and auditing.